Vinovest Quarterly Report Q4 2024

The last months of 2024 were as complex as they were pivotal: short-term price pressures but resilient trade volumes in wine, a renewed focus on fundamentals in whiskey, and an industry-wide brace for geopolitical changes.

Here's how wine, whiskey, and the broader landscape fared in the last months of 2024.

Further reading

Catch up on last quarter's report here.

Fine Wine Performance in Q4

It was Nathan Rothschild—financier, businessman, and father of the founder of Château Mouton—who gave contrarian investors their motto: “the time to buy is when there’s blood in the streets.” Whether he would extend that sentiment to today’s fine wine market (or whether he truly uttered those words in the first place) is anyone’s guess, but it’s hard to deny the aptness of the observation. The fine wine market continued its decline in Q4 of 2024, but with buyer pressure mounting even as sellers hold out on pricing, investors eager for the watershed moment of the final corrective downturn may not be holding their breath for long.

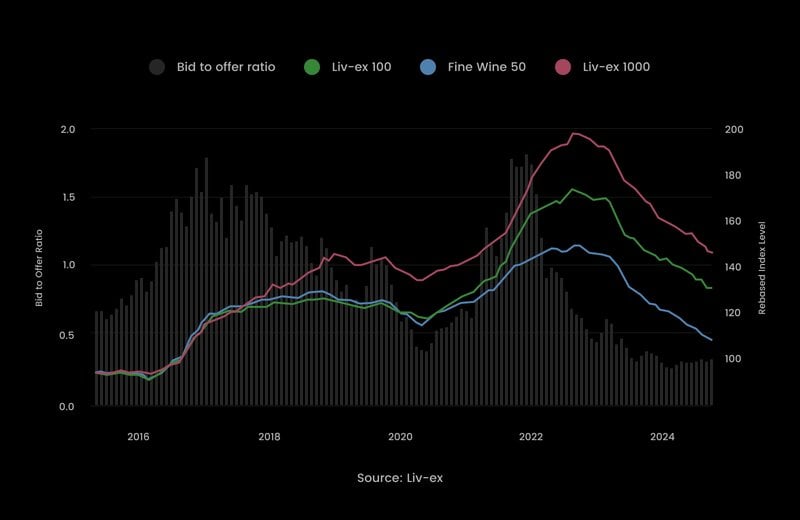

The Liv-ex Fine Wine 1000 index, a benchmark for the industry, dropped by 3.04% in Q4 2024, while the Liv-ex Fine Wine 100 index saw its greatest one-month fall of the year (2.46%) in November.

Market activity, however, did not see a similar slump: November saw the second-highest monthly trade volume of 2024. Interestingly, the share of seller-initiated trades crept upwards as well, signaling that (perhaps in anticipation of year-end), merchants were hoping to clear out stock and more willing to come down to buyer’s bids.

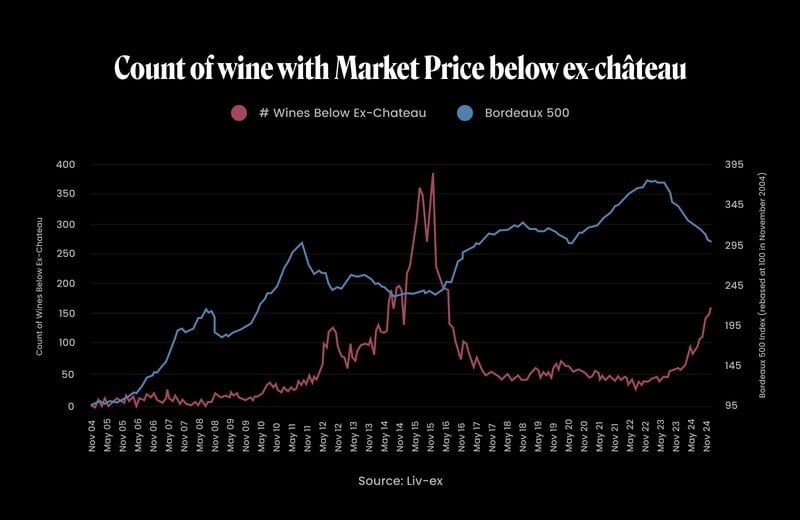

This price pressure dynamic has been ongoing throughout Q4. For example—as we noted in our November newsletter—a growing number of Bordeaux wines, especially from post-2015 vintages, are trading below their ex-château release prices on the secondary market:

“Château Lafite Rothschild, having only two labels, stands head and shoulders above any other brand in terms of both volume and value traded this year,” says Robbie Taylor, Head of Trading, APAC and Global. “It saw 22.1% more volume traded than Château Pontet-Canet and 89.3% more value than Château Mouton Rothschild. And yet, its Market Price has dropped by an average of 18.1% (across all vintages traded this year). Intuitively, healthy demand should somewhat protect prices – if volumes traded increase and prices stabilize, the market may have found an equilibrium price level. An increase in trading volumes as prices continue to drop, however, may instead indicate a growing need to offload stock.”

“What we have noticed is that there's still a high volatility going on generated by several wine suppliers and producers who are still underselling their wines on the exchange below fair market value,” adds Enrico Bresciani, Senior Portfolio Manager. “There’s essentially a delay in liquidation as the queue is moving slowly, so prices are still not realistically reflecting on the exchange.”

All told, the strategy remains the same: buy and hold. Current trading prices are more a reflection of the particulars of the present trading environment and much less a benchmark for any wine’s intrinsic value or potential.

Q4’s price movements were compounded by a continued softening of demand. Looking at one metric, the bid-offer ratio—the balance between buying and selling interest for a given wine or region—can reveal something of market sentiment, with a higher ratio suggesting stronger demand relative to supply (a seller’s market) and a lower ratio suggesting excess supply with lower demand (a buyer’s market). Throughout 2024, the overall bid-offer ratio for the Liv-ex exchange remained below 0.5, aligning with the trend and pointing to a possible need for sellers to lower their offers further to attract buyers and clear stock.

Regionally, Bordeaux indices—the Bordeaux 500 and Bordeaux Legends 40—saw sharp declines in bid-offer balance, and the Burgundy market faced challenges as well, with the Burgundy 150 index ending the year with a slim ratio of just 0.16. Unsurprisingly, the Italy 100 index fared better by this metric, with its bid-offer ratio reaching its highest point in the past year; Masseto in particular stood out with an exceptionally high bid-offer ratio, indicating strong demand and upward price pressure. And, at the level of individual wines, there were bright spots even in struggling regions like Bordeaux: wines with a strong reputation for quality and drinkability saw stable or even rising bid-offer ratios, emphasizing the power of consumer preferences in the face of broader market trends.

Sheer demand wasn’t the only metric working in Italy’s favor, either. The Italy 100 index, while down 6% year-to-date, was comparatively resilient as a sub-index, and trade activity for Italian wines was robust, with trade count, volume, and value all showing increases—driven in part by US buyers, whose strong demand for Italian wine led to a 69.3% year-on-year increase in purchase value. Within Italy, Tuscan wines continued to perform well in Q4, with trade value increasing 16.1% compared to 2023; Super Tuscans like Masseto and Soldera in particular saw significant increases in trade value, while Sassicaia, though produced in higher volumes and trading at moderate prices, also performed well, with the 2020 and 2021 vintages ranking among the top-traded Italian wines by value.

“The silver lining in the overall market picture is that Vinovest has deliberately bought volumes of Sassicaia, Tignanello, Bollinger, and so on in the knowledge that these are the most traded wines,” says Robbie Taylor. “When the market turns around, we are in a good position to see gains.”

As we enter 2025, geopolitics and the global economy are certain to be factors in the unfolding of the fine wine market correction—but when, and to what extent, remain to be seen. American buyers, buoyed by the strength of the U.S. dollar, were major players in 2024, accounting for 35.5% of fine wine purchases, but the potential tariffs on imported wine foreshadowed by the Trump administration is expected to have a cooling effect on demand (with some US merchants importing stock ahead of the incoming administration as a precaution).

Likewise, monetary policy and exchange rate fluctuations may offer some relief: lower interest rates, potentially increasing discretionary spending, could have a positive impact, even in the face of potential tariffs.

Overall, the industry sentiment is cautiously optimistic: a survey of wine professionals in December found that nearly two-thirds anticipate market growth in the next year, especially in high-end Italian wines, and our team is inclined to agree.

“Over time, we can expect a return to the mean as the queue recedes,” says Enrico Bresciani. “It's a slow process but a steady and positive trend, one that will hopefully bring prices back to their normal standards in 2025. All other pieces of the puzzle for the wine market to come back are in place: the dollar gaining strength, cuts in interest rates, China investing again. Now it's just a matter of time before we see the market react.”

Moreover, producers are likely to be under pressure to reduce release prices to stimulate the market, and all eyes are on Bordeaux and its upcoming en primeur to see how the chips fall. The small 2024 Bordeaux crop that resulted from what has been called an “annus horribilis” of weather conditions likewise presents an opportunity for producers to reset prices and regain goodwill—it is, once again, simply a matter of when.

Some two centuries after Nathan Rothschild’s heydey, it’s worth noting that his (potentially apocryphal) bon mot is sometimes recorded as a two-parter: “the time to buy is when there’s blood in the streets, even if it’s yours.” Through that lens, buyers, producers, and investors alike, no matter how bruised they may feel, could see this present moment as an opportunity (perhaps with Warren Buffett’s less-gory spin on the same idea: “be fearful when others are greedy, and greedy when others are fearful”).

Q4 Wine Exits

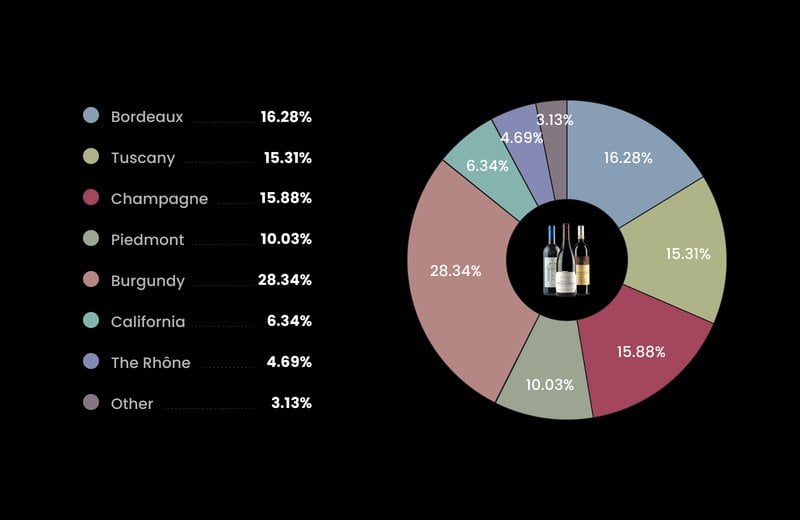

As elsewhere, Italy gained ground relative to Bordeaux in our Q4 wine exits, narrowing the gap considerably between the two powerhouse regions:

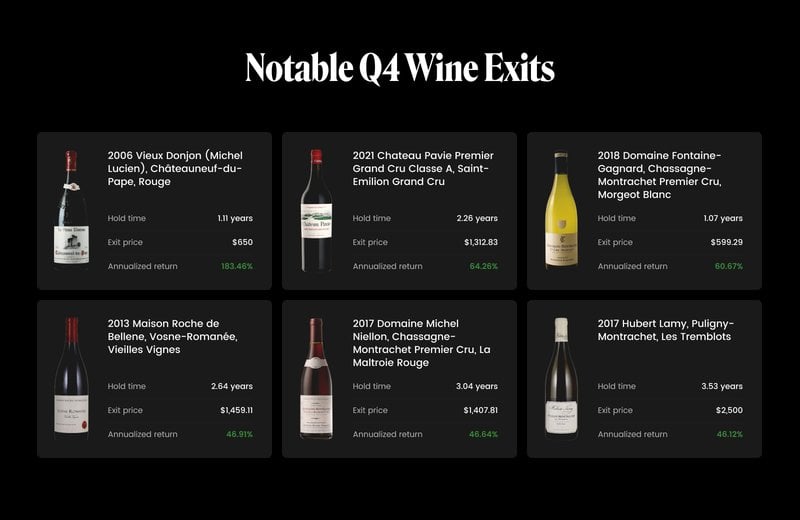

Looking at notable exits in Q4, Burgundy was a consistent performer, but a selection from the sleeper-hit Rhône region makes a strong showing as well:

Fine Whiskey Performance in Q4

In the world of whiskey, the final months of 2024 were marked by industry-wide introspection. The U.S. whiskey market headed into a correction as consumer volumes slowed, while the rare whiskey market was faced with a decline in auction sales volume and value.

With that in mind, for investors—and Vinovest clients in particular—there is every reason to remain confident in what the future holds.

First, a look at the broader market picture. The correction in the whiskey market is just that: a correction, a shift away from a market dominated by speculation-driven overstocks and companies carrying surplus inventory towards one focused on long-term value and steady appreciation. As such, it represents less a genuine free fall (or, in the colorful language of headline writers, a “hangover”) and more of a winnowing down. As the well-worn Warren Buffett quote goes, a rising tide lifts all boats; it’s only when the tide goes out that you see who’s been swimming naked.

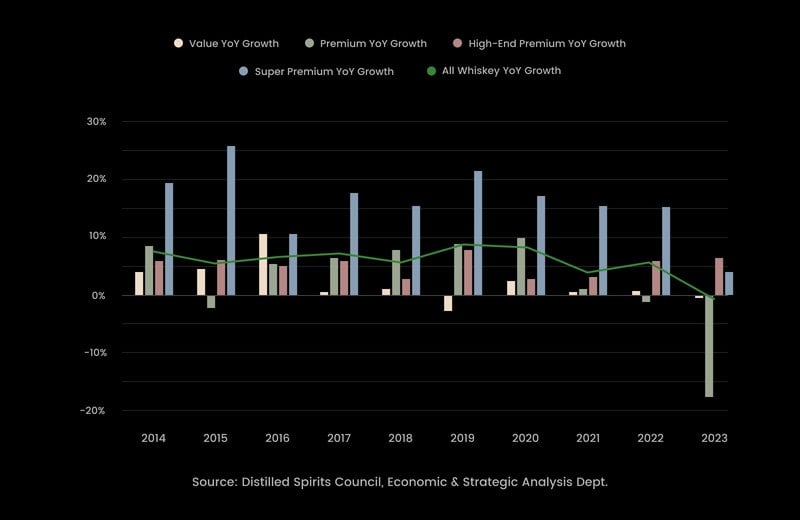

One under-reported aspect of the “soft” market for American whiskey in particular is the fact that not all American whiskey is created equal. Different tiers have grown at different rates, and the potential (and pitfalls) of whiskey investing comes with understanding these nuances. High-end premium and super-premium American whiskies were behind the skyrocketing growth during (and even before) the pandemic. The premium tier, by contrast, enjoyed a briefer pandemic boost that saw it stay fairly flat prior to 2023’s sharp correction, while the value tier by and large held at a plateau.

Moreover, super-premium American whiskey in particular shows signs of maturation. Its 2023 YoY growth of 4.0%, while a far cry from its double-digit heyday (e.g., +22.2% in 2019, +17.4% in 2020), is settling towards the compound annual growth rate of the whiskey market as a whole over the past 20 years (4.30%), suggesting that this segment could be on the path from market outlier to core contributor:

The takeaway? Selection and selectivity matter more than ever. A major advantage for our investment clients has always been not just our access to top-tier whiskies, but our selectivity in which of those whiskeys we deem worthy of portfolios. Over the past six months, we’ve focused on just a handful of key partnerships, including with storied distilleries like Kentucky’s Green River Distillery and Scottish legend Tullibardine. For those entering the market recently or in the near future, your whiskey holdings are the result of that focused and targeted approach.

It’s also worth bearing in mind that outsize growth in any sector—such as we saw in whiskey during the COVID-19 pandemic—tends to draw in a wave of opportunists, but the inevitable return to sustainable market conditions will discourage them off of the playing field. (Many whiskey "flippers" who sought quick profits by buying and quickly reselling bottles, for example, have retreated.)

In the cask market, newer or overleveraged players are finding a slower retail environment particularly hard to weather. Those who bet on rapid price increases in a short timeframe or were otherwise underprepared for the unique cash-flow rhythms of the distillation business found themselves uniquely vulnerable to a drop in demand, and while smaller or newer distillers facing difficulties selling their young bourbon barrels are indeed fighting an uphill battle, those challenges do not necessarily reflect the overall health of the entire whiskey market. (As one online commenter put it, “Demand for 2-year bourbon from a small distillery doesn't seem like a great barometer.”)

This underlines the importance of having an exit strategy in place—another focus for us in Q4. Over the past months, we were able to secure several buyback commitments with distilleries at 3, 4, 5, and 8 year intervals, locking in a buyer well in advance of the whiskey actually going up for sale. In 2025 and beyond, we plan to continue pursuing those kinds of commitments.

Finally, whiskey’s fundamental resilience remains unchanged: its inherent time horizon and exit flexibility, combined with the intrinsic value of a physical good, reward patience. When your asset not only requires aging to be sold, but improves the more it is aged, a soft market today, or even over the next few years, is all but immaterial. (This is also a factor in weighing the relative impact of tariffs: a Bourbon distilled today won’t be bottled, let alone sold to a consumer, until well into the next U.S. presidential administration.)

Making the most of these long hold times means a storage strategy that is set up for success, and to that end, we made behind-the-scenes optimization a priority in Q4 as well. One new option for investors is the ability to buy barrels with the intent to refill and reuse them for new fills. Since the barrels themselves represent a considerable part of the initial investment into a cask, this option will allow clients to hold subsequent whiskey investments at a lower cost basis. (It’s more environmentally sustainable as well.) We’ve negotiated with our partners across the supply chain so that we can offer insurance and storage fees that are as low “as humanly possible.” Finally, we completed a physical audit of our system to ensure all client portfolios accurately reflect their holdings, from valuation to mash bills.

In the long run—and whiskey investment is always in the long run—this correction is likely to be what allows the market to stabilize at more sustainable levels. Seasoned spirits business players recognized the boom for what it was—an unusual spike in demand spurred on by unprecedented consumer circumstances—and looked, as always, to the longer term and bigger picture: “every period of disruption provides opportunities,” Pete Marino, president of Bardstown Bourbon. “We’re investing through the downturn.” (It’s worth noting that Bardstown, the largest contract distiller in Kentucky, had a banner year in 2024, selling out its contracts and hiring on new staff.)

The market fundamentals are still in place, demand for high-quality whiskey persists, and long-term growth potential remains. As the tide ebbs and flows, strategy, selectivity, and insight will be the differentiators—all of which we put into practice for every portfolio.

Q4 By The Numbers

-4.79% - The average return for Vinovest-managed portfolios in Q4

-3.04% - The average return for wine on the Liv-ex 1000, an index that tracks 1,000 of the most investment-worthy wines in Q4

22 - The number of Italian wines in the 2024 Liv-ex Power 100 ranking of most- and highest-trading brands, an all-time high for the region

25 - The number of Bordeaux wines in the 2024 Liv-ex Power 100 ranking, a tie for all-time low for the region

2150.5% - As of 2023, the 20-year revenue growth in super-premium whiskey

Investing Outlook for 2025 Q1 and Beyond

After a final quarter full of twists and turns in 2024, will 2025 set a course onward and upward? We sat down with Olivier Bouchard, Winery Relations Manager, and Robbie Taylor, Heading of Trading, APAC and Global, for their forward-looking insights.

What is the market sentiment like in fine wine?

Robbie Taylor, Head of Trading, APAC and Global: The market has certainly taken a bit of a turn, but that is the reality of a market, and we’ve just got to hold tight. When you’re meant to be in it for 10 to 15 years, as you are in fine wine, you don’t really want boom and bust—we love the boom days, don’t get me wrong, but really what we hope for is a sustainable global market that is priced on par across the board. What we’re likely to see moving forward is slower increases, but more sustainable ones—hopefully nice organic growth.

Olivier Bouchard, Winery Relations Manager: There are deals to be made, to be sure, but many of the chateaux are in a mentality from the ‘70s or ‘80s when it comes to pricing—basically, that if people buy the wine, the price is not high enough. That, combined with the quality of the 2024 vintage, might get things to a tipping point.

Speaking of prices, we saw an unusually high number of wines trading below ex-château prices at the end of last year. Do you think en primeur will have reached a breaking point this year?

Olivier: Things are certainly moving in Bordeaux. We will look very carefully at how things unfold this year.

Robbie: If the Bordelais go back to pricing correctly, then we hope to see a revival. But with too many burnt fingers, buyers are rightly cautious. With increased costs and interest rates, I can’t see it happening anytime soon, though.

Italy and Spain both had a surprisingly strong showing in 2024’s Liv-Ex Power 100, with Italy taking 22 spots and Vega-Sicilia taking the top spot. Is that a sign of things to come in 2025?

Olivier: Vega Sicilia has shown solid market resilience and looks to be a solid pick going forward. As for Italy, we have to look at individual cases but there are some opportunities out there for the taking.

Robbie: A healthy diversification of the market is always a good thing. Seeing wines from Italy and Spain trading well shows that buyers are looking elsewhere and are finding value in other regions.

What else is on your mind?

Olivier: If you have been thinking about diversifying some of your portfolio into whiskey, I say do it. There is some exciting opportunity there.

Robbie: I am excited to see the market bouncing back. Albeit in a cautious and measured manner. But this is what we need. There’s still plenty of business and sales happening, but what’s interesting is that it’s not centered around French wines.

Right now, in the present conditions, you’ve got to look at everything from an individual perspective. You can't say “I’m just going to buy Burgundy” and leave it at that. My recommendation would be much more on looking at a select portfolio of top names, wines that we know that there is a solid market for. In a word: focused.

The Biggest Stories of Q4

American Single Malt Gets the Green Light

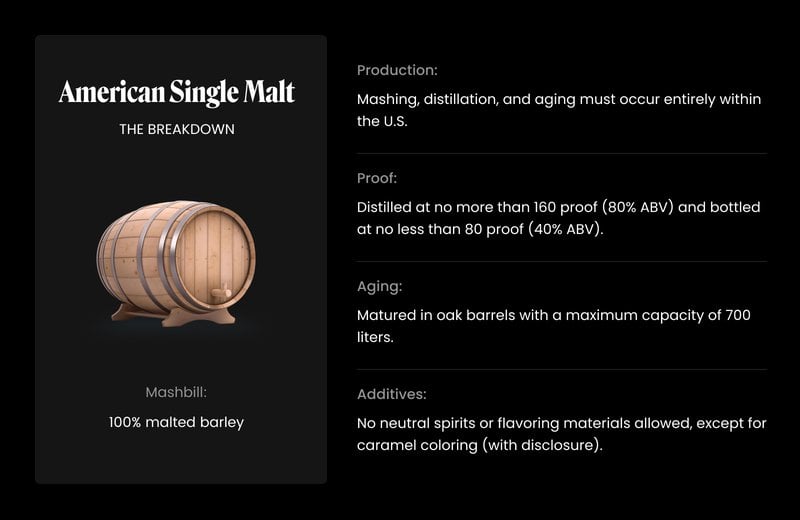

In the history of American whiskey, it’s December 5—the anniversary of the ratification of the Twenty-First Amendment, which repealed the much-less-popular Eighteenth Amendment prohibiting the sale or manufacture of alcohol—that’s long been a landmark day. This year may have just added another December date worth celebrating, however. On December 18, 2024, the Alcohol and Tobacco Tax and Trade Bureau (TTB) officially recognized American Single Malt Whiskey as a distinct category with regulated standards of identity.

With TTB designation, American Single Malt joins the ranks of bourbon whiskey, rye whiskey, malt whiskey, wheat whiskey, and corn whiskey—as well as Tennessee, light, blended, and spirit whiskey—that are defined by specific production methods, mash bills, aging requirements, and barrel types.

The story of American Single Malt Whiskey is a truly, well, American one, with roots in tradition but an innovative spirit: in 1996, Steve McCarthy, the “godfather” of American Single Malt, crafted his McCarthy’s Oregon Single Malt, inspired by Scotch Lagavulin 16 but distilled from ingredients from his native state (including locally-brewed smoky beer and barrels made from garryana oak). “He didn’t understand he was launching a category,” Joe O’Sullivan, Master Distiller at Clear Creek, recalled years later. “He wasn’t trying to disrupt the category. He just had a passion about it.”

What began as a niche labor of love quickly grew—and found market share. But even as “American Single Malt” found its way to more and more labels, the term lacked a formal, consistent definition, which left both producers and consumers in a gray area of uncertainty around quality and consistency. Then, in 2016, the American Single Malt Whiskey Commission (ASMWC) formed to spearhead efforts to secure legal recognition. It was this group’s efforts that culminated in the TTB’s decision, which took effect just a few days ago on January 17, 2025—the first new whiskey category added to U.S. regulations in over 50 years (the last one being light whiskey, in 1968).

The official recognition of American Single Malt Whiskey is more than a routine regulatory rubber-stamping, however: for many U.S. producers, it’s a point of pride. “If we want to be taken seriously along with single malt producers from Scotland, Ireland, Japan, etc., we need to have a well-defined and official place in the American marketplace,” said Mark McLaughlin, co-founder of Old Line Spirits. “An official category designation gives the ASM category an added element of legitimacy.”

Legitimacy—and opportunity for market share. American Single Malt has long outgrown the domain of smaller producers, with bigger names like Jack Daniel’s, Jim Beam, and Bulleit all having released their own spin (albeit prior to the official designation). In the month and change since the TTB’s decision, meanwhile, several producers have already seized the moment and leapt into the category (North Carolina’s Southern Distilling Company, for example, announced plans to produce over 20,000 barrels of American Single Malt under its contract distilling program).

Sadly, one person will not be toasting the triumph of December 18: Steve McCarthy, the American Single Malt “Godfather,” who passed away in 2023. “Steve would look at American single malt now and realize it was living a larger life than he ever allowed himself,” O’Sullivan said. “Being the beginning of it is very special.”

En Primeur Awaits a Reckoning

En primeur, the centuries-old tradition of buying wine while it’s still aging in barrels, has long been central to Bordeaux’s wine market. Rooted in the 18th century, this system allows collectors and investors to secure allocations of prized vintages early, often with the promise of favorable pricing, and it’s historically been a win-win for producers and collectors alike. Yet, as the wine industry has closed out 2024 and now looks to the 2025 campaign, en primeur faces a reckoning.

An almost perfect storm of challenges looms. The state of the 2024 vintage is the most obvious issue: difficult weather conditions led to a lackluster harvest unlikely to match the quality of standout years like 2010, 2016, or 2019. And while a middling vintage quality would dampen enthusiasm even in the best of circumstances, there’s the compounding issue of relative oversupply of comparatively higher quality vintages. With excellent back vintages readily available at competitive prices, many investors are asking: why buy futures when you can have proven quality now?

More broadly, there’s an issue of value perception. As we noted at the time, in November 2024, some 168 Bordeaux wines were trading below their original ex-château release prices. While this trend has historical precedent (most notably in 2015 when celebrated 2009 and 2010 vintages suffered similar post-release price drops), it underscored a growing disconnect between what producers are asking and what buyers are willing to pay, and weakens the traditional argument for buying en primeur—early, one-time access.

Less measurable, but no less a factor, is a burgeoning sense of dissatisfaction. Buyers feel that some Bordeaux producers have lost credibility by overselling to the secondary market, yet refusing to adapt pricing in the face of the resulting surplus of stock, and taking an unreasonable hardline stance. (“Bordeaux,” as the New Wine Review observed, “isn’t known for charitable pricing during the En Primeur season.”) The result is something of a standoff between Bordeaux producers and buyers, and a general erosion of goodwill.

With en primeur at a crossroads going into 2025, it seems tradition alone may no longer suffice to sustain this system. As the saying goes, qui n’avance pas, recule (roughly: if you’re not moving forward, you’re falling behind) but we will certainly be looking ahead for what’s to come.

The 2025 Bordeaux en primeur campaign is scheduled to begin on Monday, April 14, 2025.

Tariffs: An Industry Forewarned is An Industry Forearmed

One topic was unavoidable for wine and whiskey investors in the final months of 2024: tariffs. The specter of impending “Trump 2.0” tariffs on imported wine and spirits—and the potential for retaliatory tariffs from the EU, among others—have sparked both strategic recalibration and heated condemnation across the industry, with producers, merchants, and investors bracing for impact.

However—as we noted in our blog post—this is not the industry’s first Trump tariff rodeo, and with a sense of what might be in store, players in all sectors of the industry are going in older, wiser, and considerably more fired-up. Here’s a closer look at how the industry’s approach has shifted from then to now—and what it means for businesses and investors.

From a cash flow standpoint, the prior round of tariffs saw many importers and distributors simply absorbing costs: hoping the tariffs would be temporary, many wine importers reduced their profit margins rather than raise prices and risk losing customers. Now, however, the approach is much more one of preparation and caution: not only has history shown that the tariffs are unlikely to be temporary, the comparatively softer market of 2025 means that many merchants no longer have the margin to take the financial hits. The upshot is a strategy of clear-eyed pragmatism: scaling back where possible and keeping balance sheets healthy.

Inventory management, too, has been proactive: with advance knowledge of a deadline, some merchants are stockpiling right down to the wire (export volumes of Italian wine, for example, shot up 41% in November, compared with just 19.5% growth for all of 2024 prior). Many whiskey producers, meanwhile, are staying the course in domestic markets, and/or doubling down on premiumization to ensure their efforts go to their most profitable product lines.

Then there’s the strategy to face the issue the American way: with lobbyists. Trade groups like the U.S. Wine Trade Alliance (USWTA) now have an administration’s worth of data about the effects of tariffs, and they’re using it in a concerted effort to educate and activate not only policymakers, but the American public, emphasizing the negative impact on small businesses and consumers alike. Even domestic producers—who could arguably be said to benefit from more expensive imported wines—are sounding the alarm, noting that many key winemaking supplies, like French oak barrels, corks, and glass, are made abroad and imported, and an across-the-board tariff would drive up costs.

Overall, the strategies for the second round of tariffs reflect a once-burned industry that is equally braced for impact and prepared to fight it tooth and nail. Indeed, some remain hopeful that—for wine and whiskey producers, at least—it will all be for naught.

“Now, I do want to say, tariffs are certain,” said Ben Aneff, head of the U.S. Wine Trade Alliance in Sacramento and the managing partner of Tribeca Wine Merchants in New York, to NorCal Public Media. “Tariffs on wine are absolutely not certain.” (As of this writing, no tariffs have been announced.)

In Case You Missed It

Last but not least, the Vinovest team finished the year strong in the media world, sharing insights into wine and whiskey trends across print, digital platforms, and beyond. Here’s a look at the highlights.

Forbes 30 Under 30: Finance

A toast to our CEO, Anthony Zhang, and his nomination to this list of young business leaders for 2024. Kudos!

Wine and Whiskey: Investing for Enjoyment and Diversification

Vinovest CEO Anthony Zhang sat down with Financial Samurai for an in-depth look at what makes wine investing particularly enjoyable.

Meet the tech entrepreneur managing more than $100 million in whisky and fine wine investments

“The DNA of the company is very different from any others out there”: Anthony, along with Head of Whiskey Rachel Hanson, took Whisky Magazine behind the scenes of our whiskey investment approach.

From Closure To Comeback: The Investment Potential Of Ghost Distilleries

What happens when legendary whiskey brands are revived years after shuttering? Opportunity (and great whiskey). Learn all about these so-called “ghost distilleries” and how they affect the whiskey market in this piece by CEO Anthony Zhang in Forbes.